|

| Harrison Barnes |

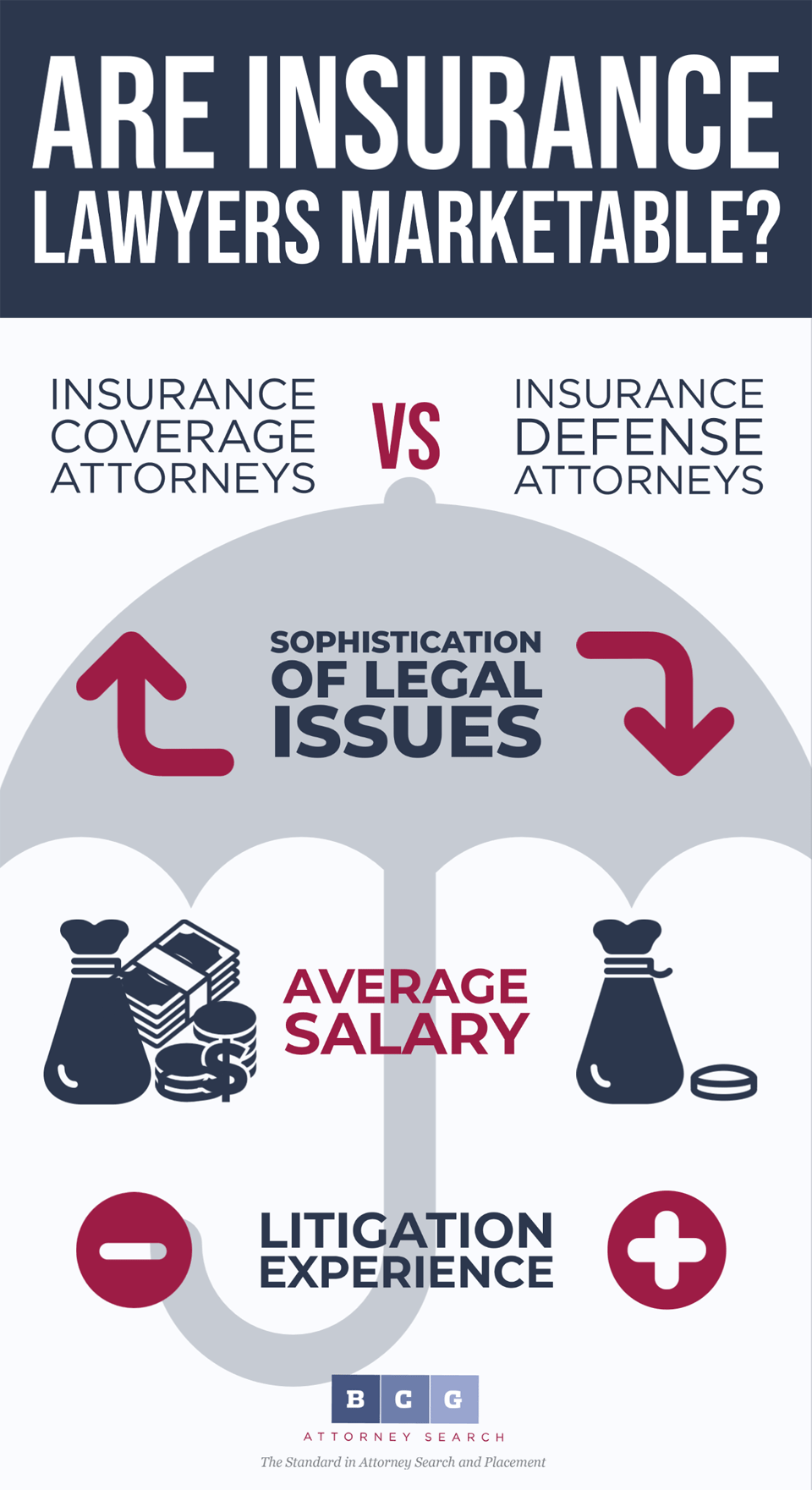

We are frequently contacted by attorneys whose practices focus on insurance law. The relative marketability of these attorneys depends on the specific nature of their practice. Insurance coverage attorneys are highly marketable, and can take up challenging new positions with top law firms with relative ease. On the other hand, those who practice insurance defense find it more difficult to make an upwardly-mobile move, notwithstanding their often excellent litigation skills.

As a general rule, insurance coverage cases involve more sophisticated legal issues and are more likely to result in binding case law that will directly affect future claims.

The phrase "insurance defense" refers to situations where an insurer hires counsel to defend its insured against an action brought by a third party -- typically, an action alleging that the insured has caused the third party to suffer bodily injury or property damage. The parties to the action typically are the insured and the third-party claimant. The legal issues revolve around whether the insured defendant is liable to the third party, and if so, for how much.

In contrast, the parties to insurance coverage actions generally are the insurer and the insured. The insured is seeking to recover under a policy of insurance, and the central legal question is whether the insured's policy covers the loss or liability. Insurance coverage actions also may involve complex issues, including disputes between insurers-relating to matters such as primary/excess coverage, time-on-the-risk, or reinsurance. Such actions also may involve first-party claims for coverage (e.g., for a loss suffered by the insured, rather than by a third party, such as fire or earthquake damage to the insured's home, or theft of the insured's personal property) that are never at issue in insurance defense.

Automobile insurance provides a fairly straightforward example of the difference between insurance defense and insurance coverage. Imagine that an insured driver is involved in an automobile accident with another driver. As a result, both cars are damaged, and the other driver is injured. The other driver sues the insured for the injuries and damages allegedly suffered. The insured therefore seeks coverage for the other driver's injuries and property damage, and asks the insurer to defend him in the lawsuit brought by the other driver.

If there are no coverage issues, the defendant's insurer will appoint counsel to defend the insured in the action, and will attempt to resolve the claim for bodily injury and property damage, by settlement or otherwise. The legal issues will be fairly straightforward -- how did the accident occur, what was the proximate cause of any resulting injuries and damage, and what is the monetary value of the injuries and damage suffered. If the insured is found liable, or agrees to a settlement within policy limits, the insurer will pay the tab.

But if there are coverage issues, the insurer may refuse to cover the damages suffered by the insured and the third party, and may refuse to defend the insured in the lawsuit brought by the other driver. In that event, coverage litigation may ensue -- instigated by either the insured or the insurer -- in which the operative question will be whether the insured's policy covers-or potentially covers-the loss or liability resulting from the automobile accident, thereby entitling the insured to a defense and/or indemnity. The legal issues involved in such a suit will not focus on whether the insured is liable to the other driver. Rather, they will focus on matters such as whether the policy was in effect at the time of the accident, whether the driver of the vehicle was in fact insured under the policy, or whether the insured's liability arises from an excluded risk (such as situations where the insured intentionally caused the accident).

Thus, insurance defense cases tend to focus on the facts of a particular incident or occurrence. Insurance coverage cases tend to focus on the language of the policy and the case law construing the policy language. Such cases can have a much more dramatic impact on the insurer's bottom line, because they can establish precedent that will apply to future claims.

Insurance defense law firms are less likely to use legal recruiters than firms that handle insurance coverage work.

While insurance defense cases sometimes involve high-dollar claims, the practice generally tends to be high volume/low value. Because insurance defense work tends to be high volume, insurance carriers often assign a lot of cases to a particular firm, but pay a fairly low hourly rate. Insurance coverage cases, on the other hand, can be quite large scale, with multimillion dollar claims that take years to litigate (for example, claims for coverage of liability for environmental contamination that allegedly took place over decades, thereby implicating numerous policies). Carriers generally are willing to pay a much higher hourly rate for these types of cases, because as a general rule, the work is more sophisticated, and, as mentioned above, more likely to result in binding case law that will apply to future claims.

Firms that handle insurance defense work tend to pay their attorneys salaries that are below market. They are often unwilling to recruit lateral attorneys through recruiting firms, which can entail a substantial fee, preferring to hire candidates directly. On the other hand, many of the top law firms in the country handle insurance coverage work. Some handle such matters on behalf of insurers and some handle them on behalf of well-heeled corporate policyholders. In either event, such firms are able to command very respectable hourly rates for their work, and generate a healthy revenue stream in the practice area. Many such firms are our clients. Attorneys weighing their long-term prospects may find it helpful to compare Commercial Litigation vs. Insurance Defense: Key Differences, Salaries, and Career Limitations for a deeper understanding of how career trajectories differ.

Insurance defense attorneys can maximize their marketability to top law firms by focusing on insurance coverage work to the greatest extent possible, and honing their litigation skills.

Many law firms that focus primarily on insurance defense work also do a fair amount of insurance coverage work. Attorneys who work at such firms can maximize their marketability to top law firms by handling as much insurance coverage work as they can get their hands on. Attorneys who have done so (including this author) have been able to leverage themselves into better-paying positions at more prestigious law firms, where they have handled more sophisticated and satisfying work. We have had success marketing such attorneys to top law firms by focusing on the strong, hands-on litigation experience that they have gained through their insurance defense work, and the exposure to sophisticated legal issues that they have gained through their insurance coverage work.

Such attorneys should approach a potential lateral move with considerable thought. Some individuals in hiring positions have a bias against insurance defense attorneys, perceiving them to be less careful in their work and to have less sophisticated experience than other candidates. To address any such bias, a candidate should ensure that his or her application is as well-presented and informative as possible. The application should highlight any insurance coverage experience-including a description of the specific nature of that experience (e.g., first-party or third-party, types of coverage/claims, etc.) as well as the extent of the candidate's hands-on litigation experience. Many insurance defense attorneys have substantially more experience than their counterparts at more prestigious firms in handling depositions, oral arguments, arbitrations, and trial. This experience can be very attractive to firms when presented as part of a strong package.

A final thought to keep in mind is that conflicts can be a major concern in insurance coverage work. While some firms represent both insurers and policyholders, most focus on representing one side or the other. A firm that represents only policyholders may be unwilling to consider hiring an attorney who has represented insurers, simply as a matter of firm policy, or due to actual or perceived conflicts of interest. Your job search should be tailored accordingly.

Any of our BCG recruiters would be happy to discuss your insurance practice with you to determine how you can take your practice to the highest level.

Click here to contact Harrison

About Harrison Barnes

The Architect of the Hidden Legal Job Market

For most lawyers, an attorney job search begins with public job postings, law firm websites, and job boards. Harrison Barnes knows that the best opportunities are often found elsewhere—in the hidden legal job market, where confidential firm needs, quiet practice expansions, and customized roles are never publicly advertised.

As the Founder and CEO of BCG Attorney Search, Harrison has spent more than 25 years helping attorneys access opportunities before they reach the public market. He understands that law firms often hire strategically and confidentially, especially when seeking highly marketable lateral talent, replacing underperformers, or expanding key practice areas.

Harrison’s insight into law firm recruiting comes from firsthand legal experience. He is a graduate of the University of Virginia School of Law, a former federal law clerk, and a former associate at Quinn Emanuel. Early in his career, he saw that traditional legal recruiting was often reactive and overly dependent on posted openings.

To change that, Harrison built BCG Attorney Search into one of the most comprehensive legal recruiting platforms in the country. Over the past two and a half decades, he has invested heavily in proprietary law firm intelligence, attorney market data, and a nationwide recruiting team. This infrastructure helps identify legal career opportunities before they become visible to most candidates.

Harrison and his team do more than match resumes to job descriptions. They help attorneys understand their legal career options, improve their marketability, and position themselves as solutions to a law firm’s specific needs. Whether advising a junior associate, a senior associate, counsel, or a partner, Harrison focuses on aligning each attorney’s strengths with the right firm, platform, and long-term career path.

Through this approach, Harrison has helped place attorneys in thousands of law firms nationwide, from Am Law 100 firms to specialized boutiques and growing regional practices. His work has helped attorneys make career moves that many believed were impossible.

Today, Harrison Barnes is recognized as one of the legal industry’s leading recruiters and career strategists. His legal career advice, articles, webinars, podcasts, and resources such as The Legal Career Insider Substack are followed by attorneys across the country.

Harrison believes the best legal careers are built by finding doors others cannot see. Through BCG Attorney Search, he gives attorneys access to the hidden market—and helps them move toward the career they truly want.

This breadth of placements is unheard of in the legal recruiting industry and is a testament to his extraordinary ability to connect attorneys with the right firms, regardless of market size or practice area.

Proven Success at All Levels

With over 25 years of experience, Harrison has successfully placed attorneys at over 1,000 law firms, including:

- Top Am Law 100 firms such including Sullivan and Cromwell, and almost every AmLaw 100 and AmLaw 200 law firm.

- Elite boutique firms with specialized practices

- Mid-sized firms looking to expand their practice areas

- Growing firms in small and rural markets

He has also placed hundreds of law firm partners and has worked on firm and practice area mergers, helping law firms strategically grow their teams.

Unmatched Commitment to Attorney Success - The Story of BCG Attorney Search

Harrison Barnes is not just the most effective legal recruiter in the country, he is also the founder of BCG Attorney Search, a recruiting powerhouse that has helped thousands of attorneys transform their careers. His vision for BCG goes beyond just job placement; it is built on a mission to provide attorneys with opportunities they would never have access to otherwise. Unlike traditional recruiting firms, BCG Attorney Search operates as a career partner, not just a placement service. The firm's unparalleled resources, including a team of over 150 employees, enable it to offer customized job searches, direct outreach to firms, and market intelligence that no other legal recruiting service provides. Attorneys working with Harrison and BCG gain access to hidden opportunities, real-time insights on firm hiring trends, and guidance from a team that truly understands the legal market. You can read more about how BCG Attorney Search revolutionizes legal recruiting here: The Story of BCG Attorney Search and What We Do for You.

The Most Trusted Career Advisor for Attorneys

Harrison's legal career insights are the most widely followed in the profession.

- His articles on BCG Search alone are read by over 150,000 attorneys per month, making his guidance the most sought-after in the legal field. Read his latest insights here.

- He has conducted hundreds of hours of career development webinars, available here: Harrison Barnes Webinar Replays.

- His placement success is unmatched-see examples here: Harrison Barnes' Attorney Placements.

- He has created numerous comprehensive career development courses, including BigLaw Breakthrough, designed to help attorneys land positions at elite law firms.

Submit Your Resume to Work with Harrison Barnes

If you are serious about advancing your legal career and want access to the most sought-after law firm opportunities, Harrison Barnes is the most powerful recruiter to have on your side.

Submit your resume today to start working with him: Submit Resume Here

With an unmatched track record of success, a vast team of over 150 dedicated employees, and a reach into every market and practice area, Harrison Barnes is the recruiter who makes career transformations happen and has the talent and resources behind him to make this happen.

A Relentless Commitment to Attorney Success

Unlike most recruiters who work with only a narrow subset of attorneys, Harrison Barnes works with lawyers at all stages of their careers, from junior associates to senior partners, in every practice area imaginable. His placements are not limited to only those with "elite" credentials-he has helped thousands of attorneys, including those who thought it was impossible to move firms, find their next great opportunity.

Harrison's work is backed by a team of over 150 professionals who work around the clock to uncover hidden job opportunities at law firms across the country. His team:

- Finds and creates job openings that aren't publicly listed, giving attorneys access to exclusive opportunities.

- Works closely with candidates to ensure their resumes and applications stand out.

- Provides ongoing guidance and career coaching to help attorneys navigate interviews, negotiations, and transitions successfully.

This level of dedicated support is unmatched in the legal recruiting industry.

A Legal Recruiter Who Changes Lives

Harrison believes that every attorney-no matter their background, law school, or previous experience-has the potential to find success in the right law firm environment. Many attorneys come to him feeling stuck in their careers, underpaid, or unsure of their next steps. Through his unique ability to identify the right opportunities, he helps attorneys transform their careers in ways they never thought possible.

He has worked with:

- Attorneys making below-market salaries who went on to double or triple their earnings at new firms.

- Senior attorneys who believed they were "too experienced" to make a move and found better roles with firms eager for their expertise.

- Attorneys in small or remote markets who assumed they had no options-only to be placed at strong firms they never knew existed.

- Partners looking for a better platform or more autonomy who successfully transitioned to firms where they could grow their practice.

For attorneys who think their options are limited, Harrison Barnes has proven time and time again that opportunities exist-often in places they never expected.

Submit Your Resume Today - Start Your Career Transformation

If you want to explore new career opportunities, Harrison Barnes and BCG Attorney Search are your best resources. Whether you are looking for a BigLaw position, a boutique firm, or a move to a better work environment, Harrison's expertise will help you take control of your future.

👉 Submit Your Resume Here to get started with Harrison Barnes today.

Harrison's reach, experience, and proven results make him the best legal recruiter in the industry. Don't settle for an average recruiter-work with the one who has changed the careers of thousands of attorneys and can do the same for you.

About BCG Attorney Search

BCG Attorney Search matches attorneys and law firms with unparalleled expertise and drive, while achieving results. Known globally for its success in locating and placing attorneys in law firms of all sizes, BCG Attorney Search has placed thousands of attorneys in law firms in thousands of different law firms around the country. Unlike other legal placement firms, BCG Attorney Search brings massive resources of over 150 employees to its placement efforts locating positions and opportunities its competitors simply cannot. Every legal recruiter at BCG Attorney Search is a former successful attorney who attended a top law school, worked in top law firms and brought massive drive and commitment to their work. BCG Attorney Search legal recruiters take your legal career seriously and understand attorneys. For more information, please visit www.BCGSearch.com.

Harrison Barnes does a weekly free webinar with live Q&A for attorneys and law students each Wednesday at 10:00 am PST. You can attend anonymously and ask questions about your career, this article, or any other legal career-related topics. You can sign up for the weekly webinar here: Register on Zoom

Harrison also does a weekly free webinar with live Q&A for law firms, companies, and others who hire attorneys each Wednesday at 10:00 am PST. You can sign up for the weekly webinar here: Register on Zoom

You can browse a list of past webinars here: Webinar Replays

You can also listen to Harrison Barnes Podcasts here: Attorney Career Advice Podcasts

You can also read Harrison Barnes' articles and books here: Harrison's Perspectives

Harrison Barnes is the legal profession's mentor and may be the only person in your legal career who will tell you why you are not reaching your full potential and what you really need to do to grow as an attorney--regardless of how much it hurts. If you prefer truth to stagnation, growth to comfort, and actionable ideas instead of fluffy concepts, you and Harrison will get along just fine. If, however, you want to stay where you are, talk about your past successes, and feel comfortable, Harrison is not for you.

Truly great mentors are like parents, doctors, therapists, spiritual figures, and others because in order to help you they need to expose you to pain and expose your weaknesses. But suppose you act on the advice and pain created by a mentor. In that case, you will become better: a better attorney, better employees, a better boss, know where you are going, and appreciate where you have been--you will hopefully also become a happier and better person. As you learn from Harrison, he hopes he will become your mentor.

To read more career and life advice articles visit Harrison's personal blog.